CRIC Québec—the tax Credit for Research, Innovation and Commercialization is the province’s new, fully refundable incentive for corporations that carry out eligible R&D and pre‑commercialization work in Québec. It applies to corporate taxation years beginning after March 25, 2025, with a prescribed form to be filed with the income tax return as part of Québec’s tax return.

This program replaces eight legacy provincial innovation measures (including various R&D wage/design credits and tax holidays for foreign experts) to simplify the regime and refocus support. It is designed to complement and not replace the federal SRED program: companies can continue to claim SRED for qualifying R&D while using CRIC Québec for R&D and newly eligible pre‑commercialization and R&D equipment costs, subject to coordination rules.

The government of Québec designed CRIC to:

Note: CRIC amounts cannot be double‑claimed with other Quebec credits, and any government or non‑government assistance reduces qualified expenditures.

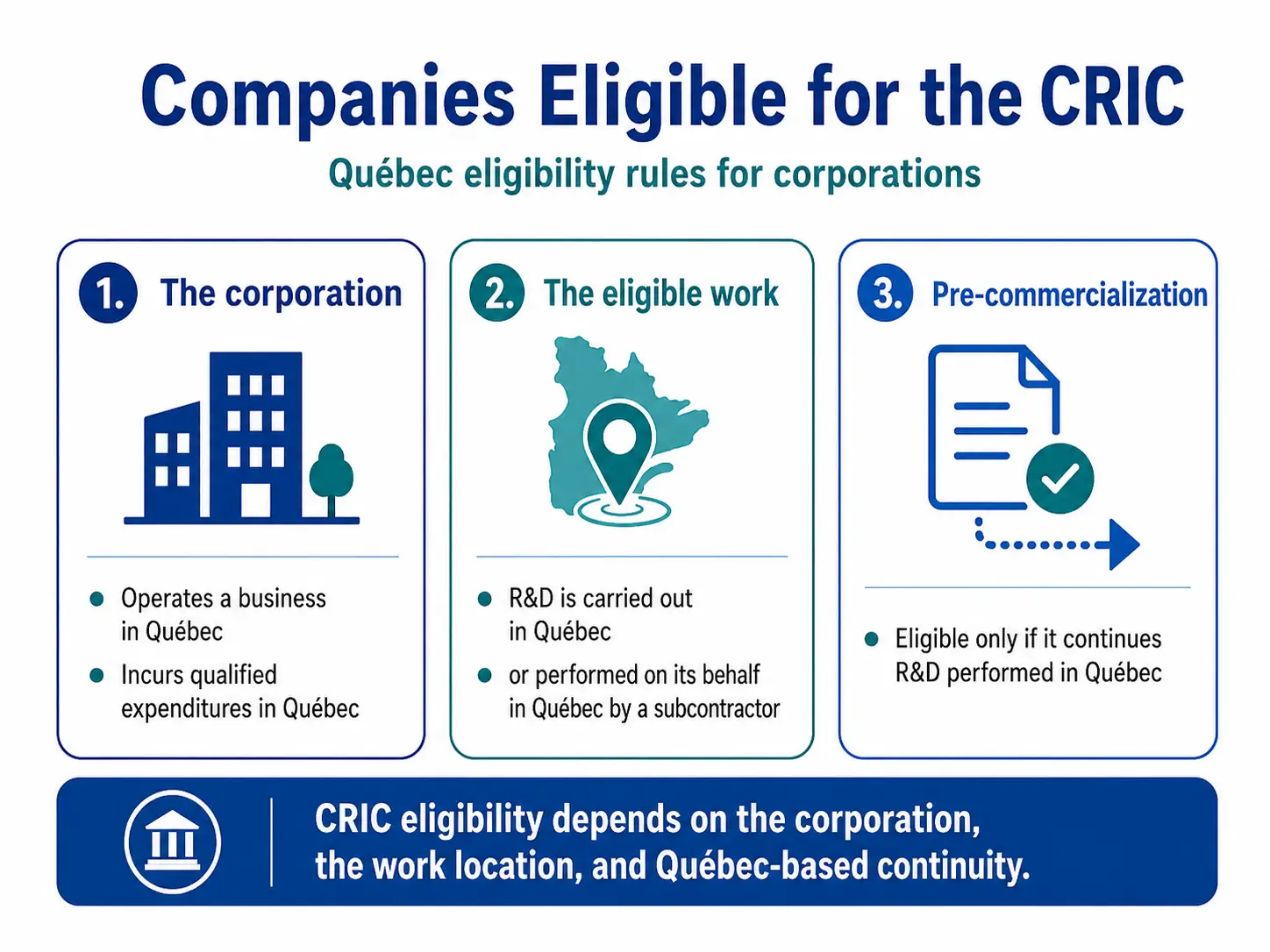

To claim the CRIC tax credit, a corporation must:

Additionally, pre‑commercialization must be a continuation of R&D performed in Quebec by the corporation or on its behalf, and qualified expenditures must be incurred in Quebec.

A Quebec corporation develops its core technology entirely outside Quebec (e.g., in Ontario or abroad). It then performs pre‑commercialization steps (certification tests, product design) in Quebec and tries to claim CRIC for those steps. Not eligible.

Why? The law requires pre‑commercialization to be undertaken in conjunction with R&D carried out in Quebec. Because the underlying R&D was not conducted in Quebec, the pre‑commercialization work fails the continuity requirement even though it happened in Quebec.

Tip: If any part of the supply chain (R&D or pre‑commercialization) is subcontracted, make sure the work location is in Québec and your files clearly show the Québec‑based continuity from R&D to pre‑commercialization.

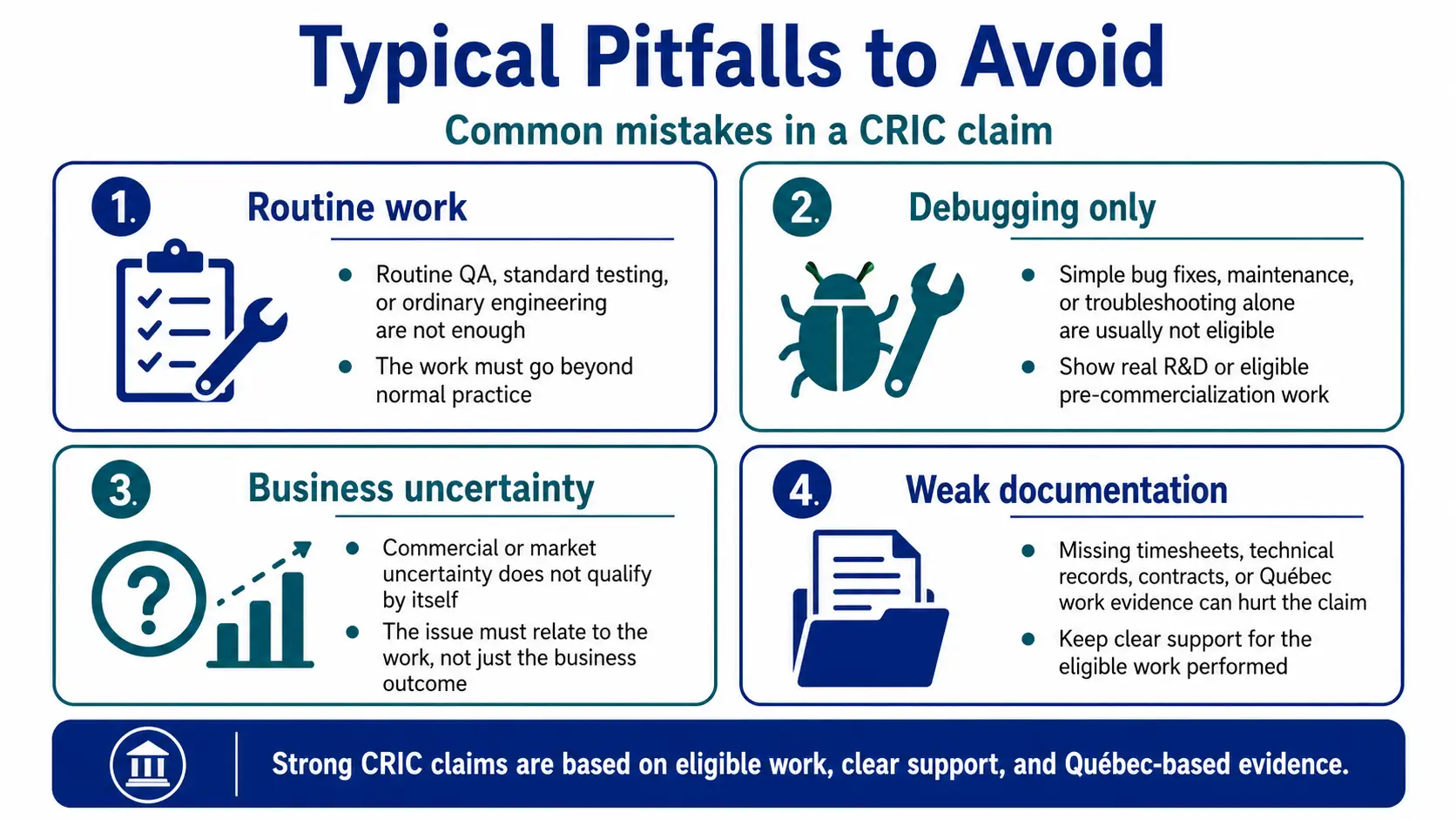

R&D activities follow the harmonized federal definitions:

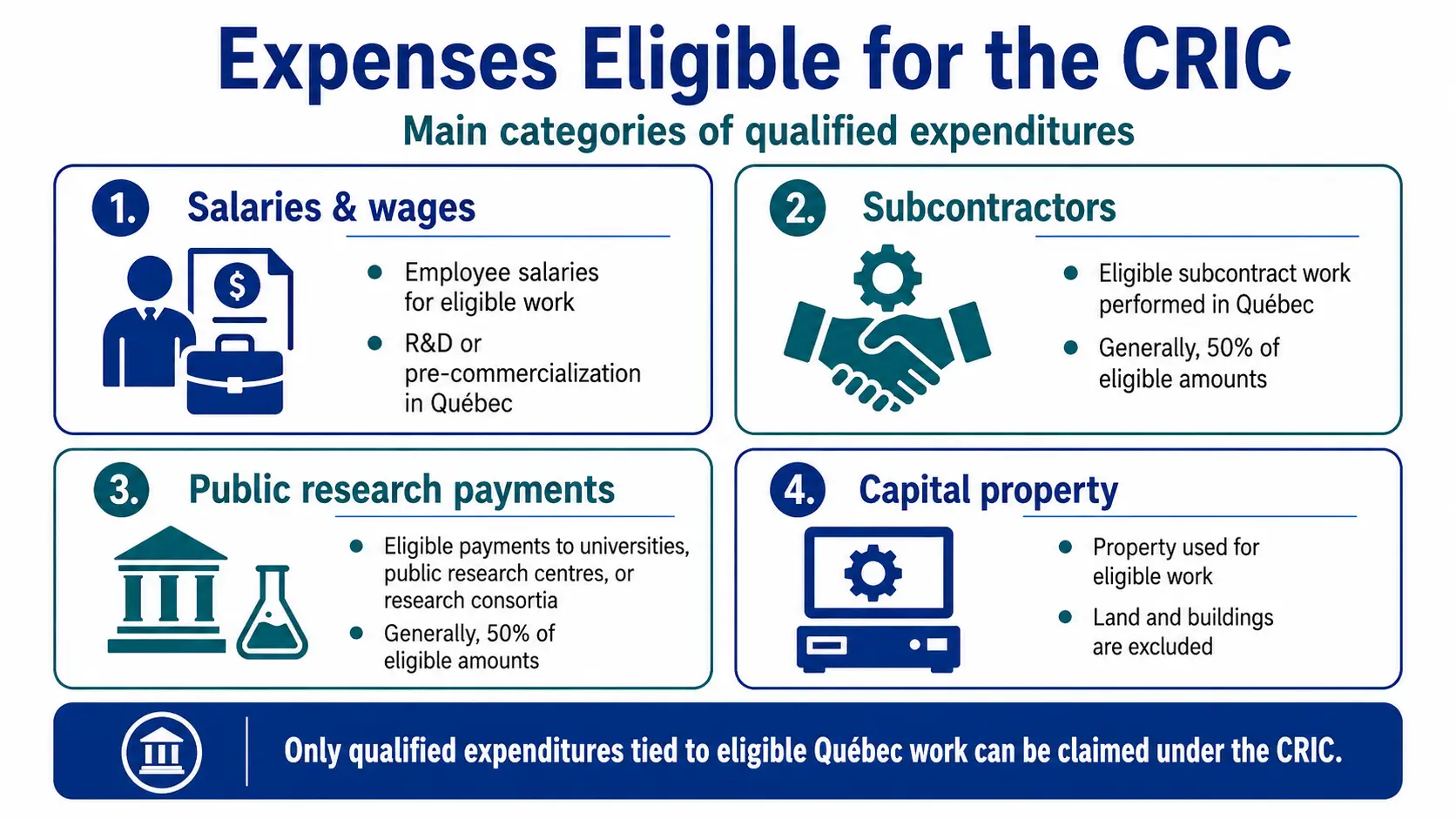

Eligible pre‑commercialization includes (CRIC Québec):

Competitive analysis of products on the market, evaluation of operational constraints, prototype development, validation by pilot users, regulatory compliance verification (e.g., health), and development of usage scenarios (use cases), where these activities are carried out directly as a continuation of R&D performed in Quebec (including subcontracted work).

Qualified expenditures (incurred in Quebec) include:

The basic rate is 30% on the first $1M above the exclusion threshold, then decreases to 20% above the first $1M, regardless of the value of corporate assets.

| Range | Rate | How it applies |

| First $1M of qualified expenses | X 30% | Applies to both R&D and pre‑commercialization |

| Excess over $1M | X 20% | All refundable credit; no asset‑size test |

| Exclusion threshold per employee | $18,952 | Portion of each employee’s salary that is not eligible for the credit. Basic personal amount for 2026, increasing every year. |

You must first exceed the greater of:

A team has 5 employees earning $80,000 each, averaging 75% of their time on R&D eligible work. The employee-based threshold is 5 X 75% X $18,952 = $71,070 (which is greater than $50,000).

With qualified expenditures of $300,000 (= 5 X $80,000 X 75%), the CRIC base is $300,000 − $71,070 = $228,930, and the credit X 30% = $68,679.

If we multiplied that team by 5 to reach 25 employees instead, the qualified expenditures would reach $1.5 M – (25 X $18,952) = $1,144,650 and the credit would be 30% on the first $1M + 20% on the rest : $1M X 30% + 144,650 X 20% = $328,930.

Bottom line: The definitions are shared and look simple, but interpretation is nuanced. With expert design up front, you protect your SRED and maximize your CRIC Quebec claim.

Unsure whether your work qualifies for tax credits or pre‑commercialization under CRIC Quebec? Call 514‑765‑3333 or email info@emergex.com for a clear, second opinion and a deeper explanation tailored to your projects.

We regularly support projects in experimental development, artificial intelligence (AI), and complex software. We also partner with accounting firms when needed to align tax and technical narratives.