The Scientific Research and Experimental Development (SR&ED) tax credit is one of the largest government incentive programs supporting innovation in Canada. This program encourages businesses to invest in research and development (R&D) by providing tax credits or refunds for eligible activities and expenses.

Administered by the Canada Revenue Agency (CRA), the SR&ED program helps companies recover a significant portion of the costs associated with developing new technologies, improving existing products, or creating more efficient processes. With $4 billion in tax benefits awarded each year, it is the largest tax initiative of its kind.

The SR&ED tax credit can significantly reduce the cost of developing innovation. Eligible companies may receive refundable or non refundable tax credits for expenses such as employee salaries, contractor fees, materials, equipment, and overhead costs related to R&D projects.

The SR&ED program is available to many types of businesses operating in Canada that conduct eligible research and development activities. The program supports companies working to create new technologies, enhance existing products, or develop innovative processes.

According to the Canada Revenue Agency, several types of organizations may be eligible to claim the SR&ED tax credit, including, by decreasing order of financial benefit:

Canadian-controlled private corporations often receive the most generous benefits, as they may qualify for larger and refundable tax credits on eligible expenditures.

SR&ED eligibility can provide significant financial support for startups and small businesses investing in innovation.

To qualify for the SR&ED tax credit, a project must involve research and development activities that aim to achieve a technological advancement. According to the Canada Revenue Agency, SRED tax credit eligibility requires systematic investigation or experimentation to resolve technological uncertainties.

The program recognizes three main categories of eligible activities:

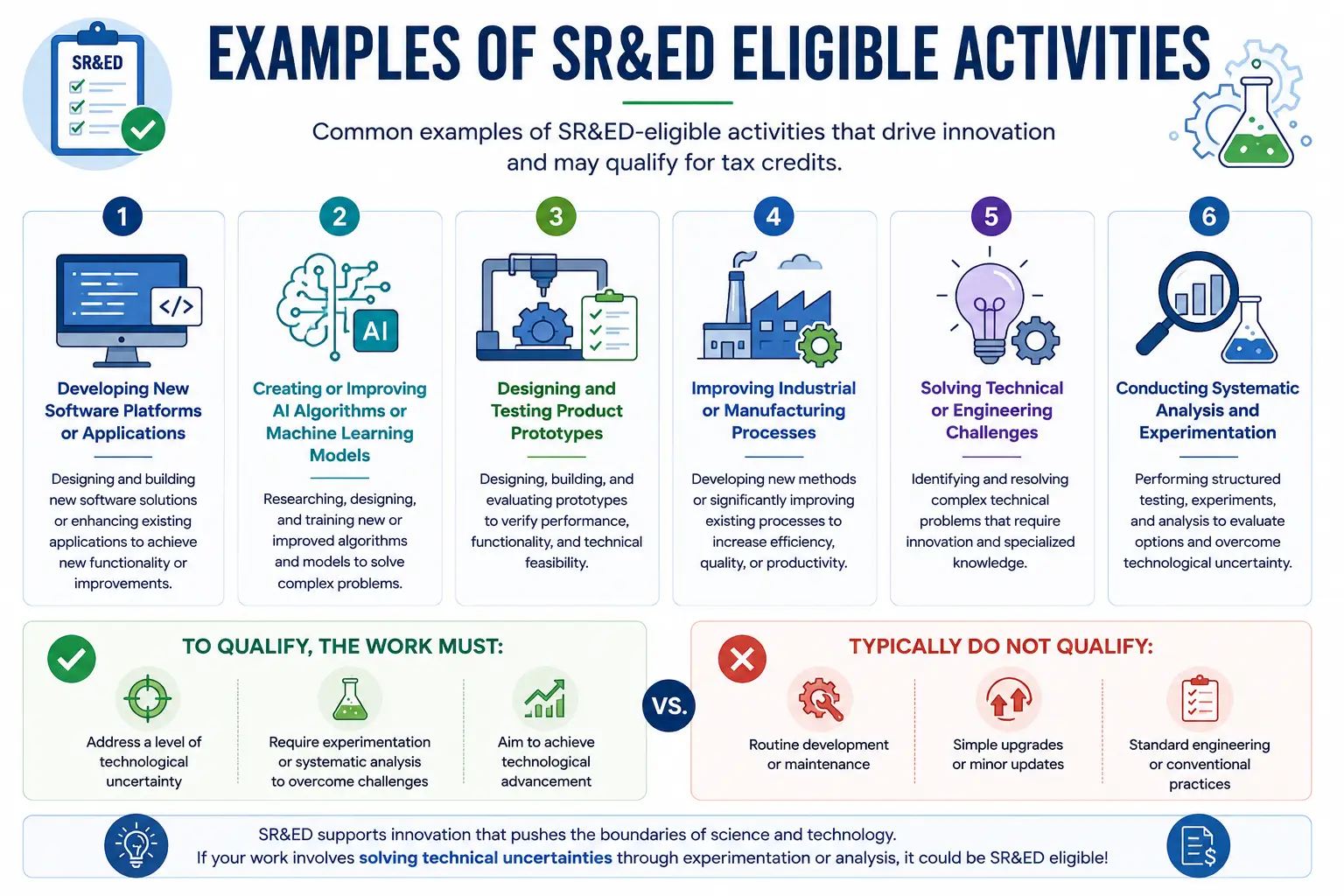

Common examples of SR&ED-eligible activities include:

To qualify, the work must involve a level of technological uncertainty and require experimentation or analysis to overcome technological challenges. Routine development, simple upgrades, or standard engineering work typically do not qualify under the SR&ED program.

Through the SRED program, your company may receive one or both of the following:

To achieve a successful claim, it is essential to maintain detailed records of your work and understand the eligibility requirements under the Income Tax Act.

Calculating your SR&ED tax credit begins by identifying eligible expenditures such as wages, contractor fees, materials, equipment, and overhead directly related to your R&D activities.

Next, determine your organization type, as Canadian-controlled private corporations (CCPCs) can access higher refundable rates, while other companies receive lower, non-refundable credits. You then apply the federal rate up to 35% for CCPCs on the first $6 million, or 15% for others—and add any applicable provincial credits.

Accurate calculation is key to maximizing your claim while staying compliant with CRA requirements.

To learn more about this, read our complete guide on how to calculate your SRED claim step by step.

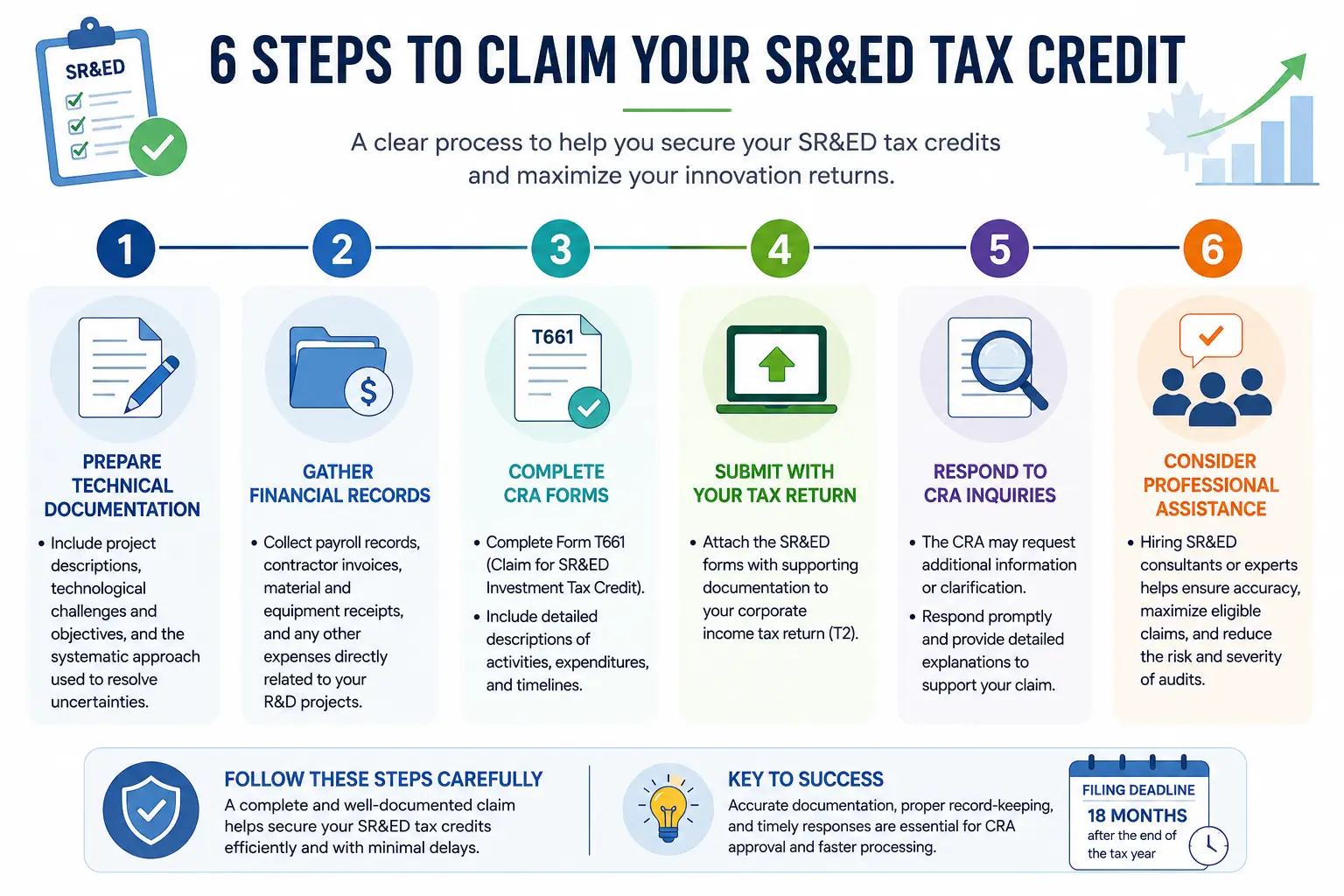

Claiming the SRED tax credit requires submitting detailed project summaries to the Canada Revenue Agency along with your corporate income tax return. Accurate record-keeping and a well-prepared claim are essential for approval.

Steps to claim your SRED tax credit:

Include project descriptions, technological challenges and objectives, and the systematic approach used to resolve uncertainties.

Collect payroll records, contractor invoices, material and equipment receipts, and any other expenses directly related to your R&D projects.

Attach the SRED forms with supporting documentation to your corporate income tax return (T2).

The CRA may request additional information or clarification. Respond promptly and provide detailed explanations to support your claim.

Hiring SRED consultants or experts helps to ensure accuracy, maximize eligible claims, and reduce the risk and severity of audits.

Following these steps carefully can help secure your SR&ED claim efficiently and with minimal delays.

Even experienced businesses can make errors when preparing an SR&ED claim. Avoiding common pitfalls can help ensure your claim is approved and maximize the tax credit you receive.

Here are some frequent mistakes to watch out for:

By avoiding these mistakes, you can improve your chances of a successful SR&ED claim and ensure your business receives the full benefits of available credits.

Emergex supports you in every phase of your SR&ED claim, from identifying eligible activities to preparing your audit defense. Our consultants ensure full compliance and are particularly experienced with IT and software development projects. Our goal is to help you maximize returns while minimizing audit risks.

Since 1994, we have helped over a thousand clients claim SR&ED credits with a 98% success rate. Our experts:

Our team ensures your qualified expenditures meet the CRA’s strict standards.

We do not just fill out forms. Emergex also provides:

Beyond SR&ED, we help you leverage other federal and provincial tax credits such as CDAEIA program, digital media, and multimedia programs. We also assist with grants like IRAP, the Industrial Research Assistance Program. Our goal is to create an optimized mix of incentives that offsets costs and supports growth.

Need liquidity before receiving your credits? Emergex helps you:

Historical success rate

Years of experience

Maximum refund with SR&ED and IRAP combined

Maximum tax refund on eligible expenses

Companies claim SR&ED every year in Canada